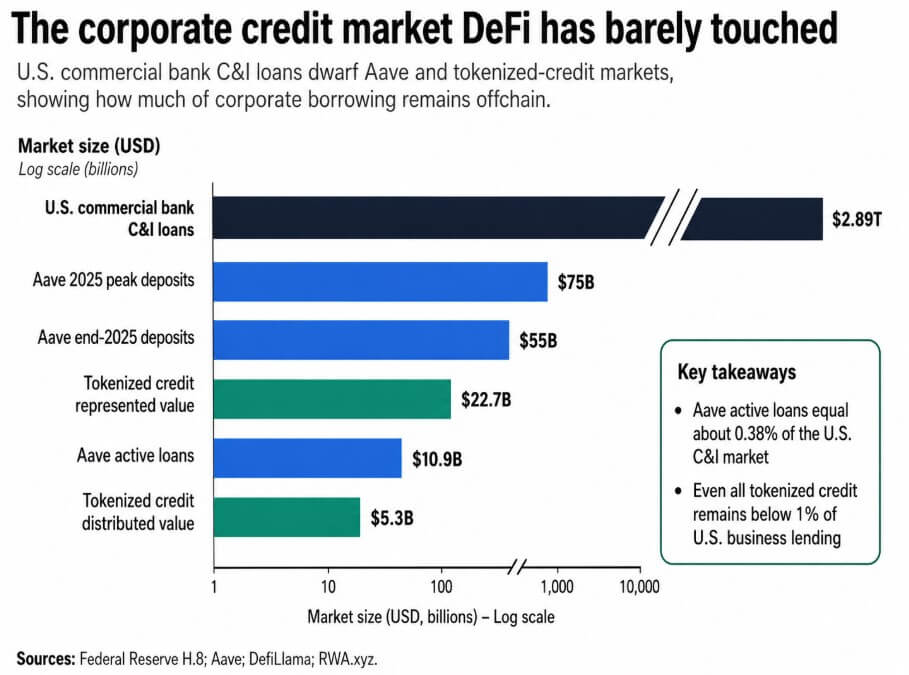

US business and industrial lending reached $2.89 trillion at business banks for the week ending Could 13, up roughly $183 billion year-to-date and eight.19% above year-ago ranges.

Company America has borrowed closely by rising charges and continues borrowing into tightening financial institution credit score situations, including extra to financial institution steadiness sheets within the first 5 months of 2026 than most DeFi protocols have ever intermediated in complete.

Aave ended 2025 with $55 billion in deposits after peaking at $75 billion, inserting it alongside mid-sized US banks by way of asset scale. DefiLlama information present its present lively mortgage guide is $10.9 billion, roughly 0.38% of the US C&I mortgage market.

Tokenized credit score throughout all on-chain platforms, together with Maple, Centrifuge, and STOKR, reaches $5.3 billion in distributed worth and $22.7 billion in represented worth, in response to RWA.xyz.

Collectively, these figures signify lower than 1% of what US banks prolong to companies alone.

The speed paradox

Aave V3 on Base exhibits a 30-day common USDC borrow APR of 4.24%, towards the Federal Reserve’s revealed US financial institution prime mortgage charge of 6.75%.

FeatureAave-style DeFi lendingBank C&I lendingWhat the lender pricesLiquid collateral riskBusiness reimbursement riskTypical collateralCrypto belongings / stablecoinsCash flows, receivables, stock, contractsMain danger controlAutomatic liquidationCovenants, underwriting, authorized recoveryRate behaviorVariable, utilization-drivenMore predictable credit score traces / negotiated termsBest borrower fitCrypto-native borrower with liquid collateralCompany looking for working capital or growth creditMain blocker for company adoptionBorrower should put up extra liquid collateralSlower, dearer, however constructed for enterprise danger

The Fed’s April Senior Mortgage Officer Opinion Survey famous that banks tightened C&I credit score requirements throughout agency sizes, raised premiums on riskier loans, and imposed stricter covenants and collateral necessities, at the same time as C&I balances continued to climb.

Aave’s borrow charge costs collateral danger, which is the price of accessing liquidity towards belongings that the protocol can liquidate mechanically, whereas a financial institution’s prime charge costs reimbursement danger based mostly on whether or not a enterprise will generate sufficient money move to service its debt.

These are structurally totally different credit score merchandise, and the 250-basis-point distance between them displays that structural distinction.

An organization usually borrows as a result of it wants capital towards money flows, receivables, stock, buy orders, or future contracts. These are the enterprise fundamentals a financial institution underwrites, and Aave can not but consider on-chain.

Aave’s personal V3 documentation describes its borrowing mannequin as all the time overcollateralized, with liquidations triggered when collateral protection falls beneath outlined thresholds.

That construction works nicely for crypto-native debtors looking for stablecoin liquidity, however leaves company debtors with out a matching product.

What the infrastructure nonetheless lacks

Money-flow underwriting requires evaluating whether or not a borrower can repay from gross sales, margins, and contracts over time.

DeFi protocols value token collateral dynamically and precisely, with no equal mechanism for assessing an organization’s income high quality or covenant compliance.

Company borrowing is beneficial exactly as a result of the borrower lacks liquid collateral equal to the mortgage quantity, and DeFi’s most battle-tested lending markets depend on overcollateralization to cut back default danger by eradicating the necessity for belief.

Actual-world collateral requires valuation, verification, custody, authorized enforceability, and restoration processes that sensible contracts alone can not execute.

Tokenized credit score platforms like Maple and Centrifuge have made progress, however their mixed distributed worth of $5.31 billion represents a fraction of the receivables-backed lending that flows by conventional financial institution services every quarter.

Aave can liquidate ETH or USDC collateral in a single block, whereas company credit score exercises contain covenants, waivers, restructuring negotiations, servicers, chapter proceedings, and courts.

Aave’s Ethereum/USDC borrow APR on Could 26 was 12.82%, in contrast with a 30-day common of 4.72% for a similar pool, which tripled over the measurement window.

A company treasurer managing a revolving credit score facility wants a predictable value of capital, and that swing makes on-chain variable credit score structurally incompatible with commonplace treasury observe.

Aave’s credit score delegation mechanism lets suppliers delegate borrowing energy to different customers, with enforcement by off-chain authorized agreements or on-chain sensible contracts, exhibiting that DeFi has the conceptual primitives for undercollateralized credit score.

It additionally exhibits why the bridge to company borrowing nonetheless runs by authorized infrastructure and off-chain belief, precisely the elements DeFi has not but automated at scale.

Two speeds

Within the bull case, tokenized collateral rails, institutional credit score managers, stablecoin settlement, and enforceable claims converge right into a functioning company credit score sleeve.

On-chain non-public credit score might attain $100 billion to $300 billion, between 3.5% and 10.4% of the present US C&I market. The trail runs by crypto-native companies and fintech lenders first, the place debtors already function in digital asset environments, earlier than increasing to conventional company debtors.

April CPI at 3.8% year-over-year, payroll development slowing to 115,000, and tightening financial institution credit score requirements create situations wherein programmable various credit score rails ought to appeal to consideration from treasury desks that already use stablecoins for settlement.

Within the bear case, DeFi serves as a strong liquidity marketplace for crypto-collateralized borrowing, whereas company credit score stays overwhelmingly on financial institution steadiness sheets.

On-chain credit score holds within the $5 billion to $20 billion vary, below 0.7% of the C&I market, as authorized, underwriting, and restoration infrastructure matures extra slowly than token markets do.

ScenarioWhat has to happenOnchain company/non-public credit score rangeShare of present U.S. C&I marketBear caseDeFi stays largely crypto-collateralized; authorized and underwriting rails mature slowly$5B–$20B<0.7percentBase caseTokenized collateral, fintech lenders, and institutional credit score managers develop step by step$25B–$75B0.9%–2.6percentBull caseTokenized collateral rails, enforceable claims, stablecoin settlement, and credit score managers converge$100B–$300B3.5%–10.4%

Banks retain the compliance, reporting, and authorized restoration equipment that company debtors require, and constructing an equal on-chain infrastructure takes longer than deploying a brand new lending pool.

DeFi has demonstrated that on-chain cash markets can deal with deposits, borrow charges, automated liquidations, and international stablecoin liquidity at a significant scale.

The subsequent alternative in company lending lies in underwriting functionality, authorized enforceability, and institutional belief.

Value Prediction 2026 2027 2028")

{kind=link}