Treasury’s first proposed GENIUS rule landed on April 1 as a discover of proposed rulemaking.

The textual content inside it builds the operational structure for US stablecoin governance, addressing which establishments might difficulty cost stablecoins, underneath what situations, and at what scale earlier than federal oversight turns into obligatory.

Why this issues: This shifts stablecoins from a fragmented regulatory patchwork towards a nationally coordinated system. For customers, it impacts how safely {dollars} might be redeemed and moved. For issuers, it defines whether or not they can scale independently or should transition right into a federal regime as they develop.

By defining when a state licensing regime qualifies as “considerably comparable” to the federal framework, Treasury is now defining these phrases.

The stablecoin market already holds roughly $316 billion, with USDT accounting for about 58% of the provision, per DeFiLlama.

Retail-sized quantity for USDC, USDT, and PYUSD grew from $500 million to $69.8 billion between 2019 and 2025. FSOC’s 2025 annual report described the GENIUS framework as a federal prudential system designed to onshore stablecoin innovation, shield holders within the occasion of insolvency, and help the US greenback’s worldwide position.

Treasury’s NPRM now exhibits how that prudential imaginative and prescient operates on the bottom.

The hidden battle over who governs

The Treasury chairs the interagency assessment committee that certifies state stablecoin regimes, which incorporates management from the Fed and the FDIC.

That committee’s judgment rests on the “considerably comparable” check, and Treasury’s proposal defines that check to incorporate the GENIUS Act itself, in addition to the implementing laws and interpretations issued by federal companies over time.

Treasury says that substantial similarity can be arduous to manage, and state and federal requirements may “starkly deviate.”

As OCC, Treasury, the Fed, FinCEN, and OFAC add implementing guidelines, the usual Washington makes use of to measure states shifts with them. State regimes authorized as we speak should observe a benchmark that Washington retains constructing.

Treasury organizes the rule round two classes. The primary, known as uniform, covers the elements that set up belief within the instrument itself: reserve belongings, redemption, month-to-month reserve publication, limits on rehypothecation, accountant examinations, BSA/sanctions compliance, lawful-order functionality, and core exercise limits.

State implementation of every uniform requirement have to be in line with the federal framework “in all substantive respects,” with no materials deviations in definitions or scope. For BSA and sanctions particularly, states should cross-reference federal guidelines instantly, with no room for state-drafted substitutes.

The second class permits calibration round some capital, liquidity, reserve diversification, danger administration, functions, licensing, and sure redemption mechanics. Treasury nonetheless constrains that room, and state decisions within the versatile bucket should produce outcomes “no less than as stringent and protecting” because the federal framework.

For instance, a state might permit extra reserve belongings provided that the OCC has already authorized them as equally liquid federal government-issued belongings. That’s federal pre-clearance administered by way of state paperwork.

CategoryRequirement areaTreasury standardState discretionWhy it mattersUniformReserve assetsMust align with the federal framework in all substantive respectsNo materials deviationDefines belief within the stablecoin itselfUniformRedemptionMust observe the federal baseline closelyNo narrower state substituteProtects holders’ potential to redeemUniformMonthly reserve publicationMust match federal expectationsVery restricted room to varySupports transparency and market confidenceUniformLimits on rehypothecationMust conform to the federal frameworkNo significant carve-outPrevents riskier use of backing assetsUniformAccountant examinationsMust be in line with federal requirementsLittle to no variationStandardizes verification of reservesUniformBSA / AML / sanctionsStates should cross-reference federal guidelines directlyNo state-drafted alternativeKeeps compliance underneath nationwide controlUniformLawful-order capabilityMust observe federal expectationsMinimal discretionPreserves enforcement and authorized accessUniformCore exercise limitsMust align with the federal frameworkNo materials divergenceKeeps issuers inside a nationally outlined modelFlexible / calibratedCapitalOutcomes have to be no less than as stringent and protecting because the federal frameworkSome calibration allowedLets states tune prudential requirements with out weakening themFlexible / calibratedLiquidityMust be no less than as protecting because the federal baselineSome calibration allowedGives restricted room for state tailoringFlexible / calibratedReserve diversificationMay fluctuate, however solely inside outcomes no less than as protecting because the federal frameworkNarrow flexibilityStates can alter, however not create a looser reserve regimeFlexible / calibratedRisk managementState framework can differ in formMust nonetheless meet protecting federal-equivalent outcomesAllows administrative variation, not a special philosophyFlexible / calibratedApplications / licensingState administration is allowedCannot create a genuinely totally different regimeKeeps the state lane administrative, not alternativeFlexible / calibratedCertain redemption mechanicsSome room to calibrateMust stay no less than as protecting because the federal systemStates can alter course of, not weaken substanceFlexible / calibratedAdditional reserve assetsAllowed provided that the OCC has already authorized comparable assetsFederal pre-clearance nonetheless governsShows state flexibility continues to be bounded by Washington

The $10 billion ceiling and what it produces

The GENIUS Act caps the state choice at issuers with not more than $10 billion in consolidated excellent cost stablecoins.

Treasury provides that state transition guidelines can not impede a transfer to federal oversight as soon as an issuer crosses that line, and issuers in a state that fails certification should both cease issuing cost stablecoins or transfer into the federal licensing framework.

The $10 billion ceiling is the structural inform, because the state lane features as an entry level for smaller issuers. At scale, the federal framework turns into the one sturdy residence.

Citi’s up to date 2026 forecast places its base-case estimate for the 2030 stablecoin market at $1.9 trillion. Commonplace Chartered projected the market may attain $2 trillion by the top of 2028.

A market at that scale runs on uniform reserve, redemption, and compliance requirements and rewards issuers able to absorbing national-style regulatory overhead.

Visa’s focus information already displays the present vacation spot: as of October 2025, greater than 97% of the stablecoin provide had converged on USDT and USDC. Treasury’s design standardizes the situations that giant, compliant issuers are already constructed to fulfill.

Commonplace Chartered estimated stablecoins may pull roughly $500 billion in deposits out of US banks by the top of 2028.

The quantity frames the context appropriately: stablecoins have gotten claims on greenback liquidity that sit alongside conventional financial institution deposits, and the establishment that governs the phrases of stablecoin issuance governs an increasing piece of greenback infrastructure.

Treasury’s proposal positions Washington as that establishment.

Scale markerAmountWhat it representsRegulatory implicationWhy it mattersState-lane ceiling$10 billionMaximum consolidated excellent cost stablecoins for an issuer to stay within the state optionAbove this line, the issuer should transition to federal oversight or cease issuing new cost stablecoinsShows the state path is a restricted entry lane, not the sturdy residence for big issuersCurrent stablecoin market~$316 billionApproximate present whole stablecoin market sizeThe market is already far bigger than the state-lane thresholdSuggests Treasury is designing guidelines for a systemically significant market, not a distinct segment oneCiti base case (2030)$1.9 trillionCiti’s up to date 2026 base-case estimate for the stablecoin market by 2030A market at this scale would possible depend on uniform nationwide requirements slightly than fragmented state variationReinforces the article’s argument that scale factors towards federalizationStandard Chartered forecast (end-2028)$2 trillionStandard Chartered’s projection for stablecoin market measurement by the top of 2028Implies that if development continues, giant issuers will nearly inevitably find yourself within the federal frameworkSupports the view that the state lane features extra like a launch ramp than a long-term alternativeBank deposit migration estimate~$500 billionStandard Chartered estimate of deposits stablecoins may pull from U.S. banks by end-2028Stablecoin issuance turns into a query of dollar-system governance, not simply crypto regulationHelps mainstream readers see this as a financial-architecture story, not a distinct segment coverage replace

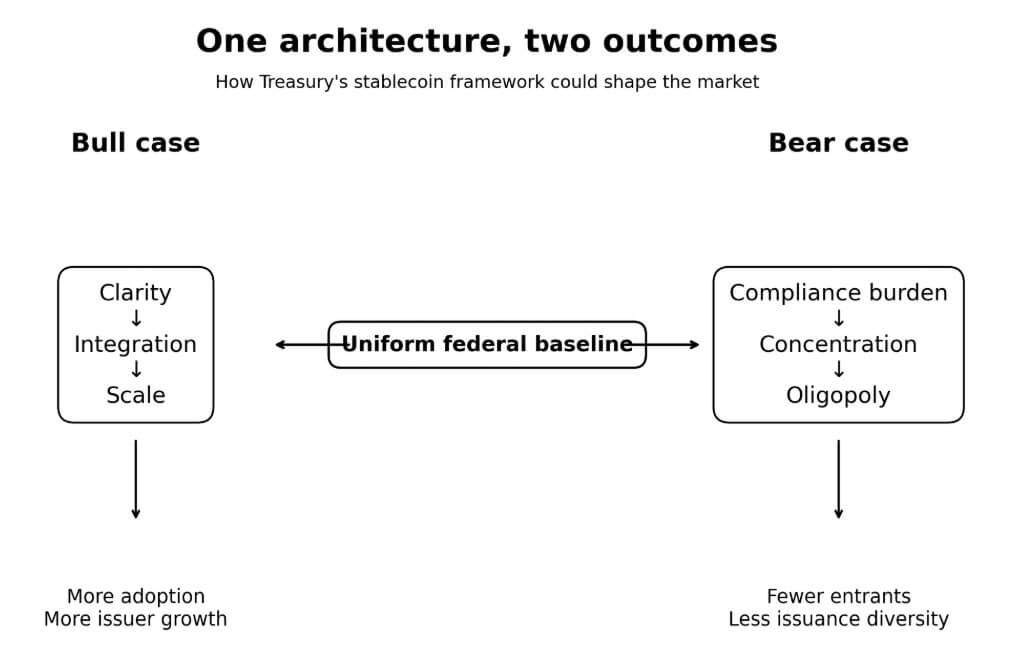

Two paths by way of the identical structure

The bull case runs from readability to scale. Uniform nationwide guidelines on reserves, redemption, and compliance take away the uncertainty that has stored banks, card networks, and enterprise treasury groups cautious about deep integration with stablecoins.

Alongside that path, provide tracks towards the Citi and Commonplace Chartered forecasts, Visa’s 130-plus card packages are overlaid on stablecoin wallets, and the state lane serves as a launch ramp for smaller issuers earlier than they graduate to federal supervision.

Treasury’s tight structure then reads because the working handbook for US digital greenback enlargement, which is a framework that made the market credible sufficient to soak up institutional demand at scale.

The bear case runs the identical structure in reverse. The forthcoming BSA/AML and lawful order guidelines, which each Treasury and the OCC have flagged as nonetheless pending in separate rulemakings, may entail heavy operational necessities.

If certification proves sluggish, pricey, or politically fraught, smaller issuers might discover the state lane functionally inaccessible even earlier than they strategy the $10 billion threshold.

The end result can be a market that’s legally cleaner however structurally oligopolistic, with innovation relocating to distribution and infrastructure, away from issuance.

Treasury frames a special objective. The predictable market response to excessive uniform compliance flooring and a tough ceiling on state-lane scale is focus, and Visa’s present market information exhibits the market was already shifting in that route earlier than the rule arrived.

Washington holds the baseline

This NPRM is an element of a bigger regulatory framework. OCC’s February proposal coated the required GENIUS laws, besides these tied to BSA, AML, and OFAC sanctions, which will probably be addressed in a separate rulemaking coordinated with Treasury.

Treasury’s personal NPRM flags that guidelines on lawful-order compliance are forthcoming as properly. The complete compliance map for stablecoin issuers awaits completion.

The $316 billion market and $10 trillion transaction quantity settled the query of stablecoins belonging within the US finance. Treasury is deciding who will get to form them as they enter it.

The primary proposed GENIUS rule makes the reply clear: Washington accepts state participation in stablecoin issuance inside a federal structure that the Treasury continues to construct, on Washington’s phrases.

Value Prediction 2026 2027 2028")

Value Prediction 2026 2027 2028")

Value Prediction 2026 2027 2028")

{kind=link}