USDC is a greenback token. XSGD is a Singapore greenback token. EURC is a euro token. The peg label solutions one query. A stablecoin rail additionally will depend on backing, issuer controls, chain deployments, switch exercise, pool counterparts, bridges, and redemption paths exterior the chain.

This follows USDC Exhibits Why Stablecoin Threat Evaluation Is Not One Sign and Native Pegs, Greenback Rails: separate the token label from the accounting and liquidity surfaces, then ask the place the money layer concentrates.

The stablecoin map appears numerous. USD, EUR, SGD, JPY, and BRL present up throughout chains and issuers. That range is actual on the label layer. It’s a lot thinner when you ask what every rail truly runs on: reserves, issuer controls, deployment alternative, switch exercise, pool counterparts, bridges, and redemption paths that largely sit exterior the chain.

I began this line of labor from a narrower fear. Geographic stablecoins are sometimes mentioned as nationwide or regional money on chain. Blockchain knowledge let me ask a more durable query. If stress hits one rail by a pool drain, bridge delay, or collateral markdown, how briskly does it transfer by a system with no lender of final resort on chain? Stablecoin depegs don’t unwind like sluggish macro headlines. They propagate by shared quote property, lending books, and bridge queues at block pace.

This put up will not be nation adoption and never reserve adequacy. It maps dependencies you’ll be able to partially see on chain: footprint, switch exercise, and DEX pool construction.

The money layer

Stablecoins settle trades, collateralize loans, bridge chains, and sit on the money leg of tokenized asset merchandise. When a market quotes in USDT, borrows in opposition to USDC, or routes by a USDC pool, the stablecoin is a part of the system’s money layer. It isn’t simply one other token.

Stablecoins additionally rely on the chain’s fuel layer. A USDC or EURC switch could also be dollar- or euro-denominated, nevertheless it nonetheless wants a local price asset to maneuver — ETH on Ethereum and lots of L2s, POL on Polygon, TRX on Tron, SOL on Solana, and so forth. The token could also be secure; the rail it strikes on will not be free.

What issues for infrastructure threat is overlap: what number of apps, swimming pools, and bridges contact the identical quote asset earlier than anybody checks reserves or redemption capability.

Footprint by peg anchor

Stablecoins are normally grouped by peg forex: USD, EUR, SGD, JPY, and BRL. A footprint map asks which rails exist, what they monitor, and the way massive their provide or market cap proxy is.

Massive footprint can coexist with skinny exercise or skinny swimming pools. The map is a list learn, not a utilization learn.

Footprint will not be switch exercise

Circulating provide measures how massive a rail is. Switch quantity measures how a lot worth moved by supported chain rails in a window. USDC and USDT dominate supported token switch quantity from 2026–04–28 → 2026–05–27. EURC reveals up; XSGD and BRLA are far smaller.

Footprint, switch exercise, and pool construction can all disagree. That’s the level: one label hides a number of dependency surfaces.

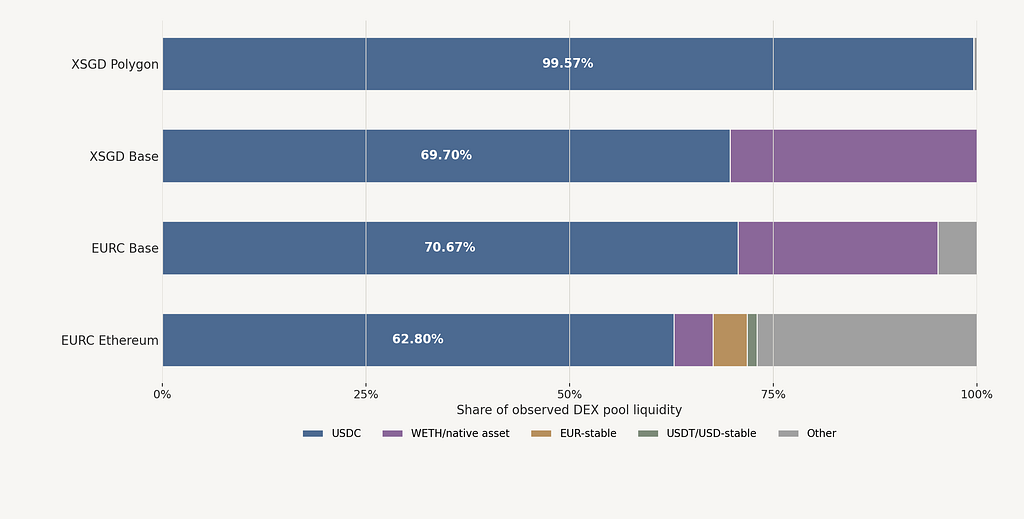

DEX pool counterparts

On a DEX, the query is what sits on the opposite aspect of the pool. I name this the pool counterpart. Within the 2026–05–29 DexScreener snapshot, chosen native forex deployments lean closely on USDC in noticed pool liquidity.

XSGD Polygon is the intense case: SGD on the label, USDC on nearly each noticed pool edge.

Interpretation: this isn’t FX range on the liquidity layer. On this chosen DEX slice, the map appears multicurrency, however the seen swimming pools behave a lot nearer to a shared greenback rail system.

One hop neighborhoods

The stacked bar reveals proportions; the one hop graph reveals form. XSGD Polygon is nearly totally linked to USDC. XSGD Base and EURC Base carry WETH/native publicity, however USDC stays the most important noticed edge. EURC Ethereum has a wider neighborhood; USDC remains to be the most important counterpart class.

Native pegs will not be floating in remoted SGD or EUR liquidity zones. On this pool graph, they sit subsequent to USDC.

What stays exterior the chain

Reserves, redemption queues, CEX order books, OTC flows, authorized claims, issuer mint coverage, and precise swap routing want completely different proof.

Tether on Omni is an early occasion of the identical break up. The token moved on-chain; balances counted; markets quoted it as a greenback substitute. The more durable query sat off-ledger: what backed it, who verified it, and what redemption seemed like when confidence broke. Switch and pool maps can’t reply that. A stablecoin is an on-chain stability and an off-chain declare.

Macro strain, reserve politics, admin controls, and contract halt rights additionally sit exterior the chain.

The map doesn’t cease at DEX swimming pools. Tokenized funds, synthetics, and pre-IPO merchandise nonetheless settle by a money leg. That leg is usually a stablecoin rail. In my earlier put up, The SpaceX Commerce Exists. Now Watch the Tape, the proof was CEX APIs, not pool liquidity: pre-IPO perps settled in USDT, with actual quantity and open curiosity, no fairness declare behind the contract.

My conjectures: native forex stablecoins could also be much less about constructing standalone nationwide liquidity on chain and extra about protecting an area unit seen on a settlement rail that also clears by greenback stock. I can’t take a look at issuer motive or macro causality from a DexScreener pull. I can examine whether or not nominally completely different pegs nonetheless share the identical pool edge. That shared edge is the place a liquidity drawback in a single token can begin to appear like a shared rail drawback.

Closing

The primary stablecoin query is what it’s pegged to. The infrastructure query is what provides it liquidity, and what else breaks when that liquidity strikes.

This snapshot reveals native pegs sitting close to USDC in noticed DEX swimming pools. That sample alone doesn’t forecast a crash. It does recommend a mismatch price taking significantly: forex labels multiply sooner than impartial liquidity rails.

The following test I’d run is swap path knowledge in opposition to the pool graph. If execution routes by USDC as typically as pool stock implies, the only rail learn will get stronger. If not, the graph overstates focus. The footprint map would nonetheless look numerous whereas execution stayed entangled.

Both approach, the dependency query comes earlier than the peg query once you care about pace. Money on chain has no quiet weekend to soak up unhealthy information.

Appendix: sources

Footprint: DefiLlama stablecoins API, which might be regenerated through `stablecoin-map-package` (beneath).Switch exercise: `ARTEMIS_STABLECOIN_TRANSFER_VOLUME`, window 2026–04–28 → 2026–05–27. Excludes CEX inside ledger movement, OTC movement, and issuer desk exercise, which might be regenerated through `stablecoin-map-package` (beneath).DEX liquidity: DexScreener pool snapshot (2026–05–29); repo artifacts stablecoin_liquidity_pairs.csv, stablecoin_pair_dependence_summary.csv. Excludes CEX depth and redemption queues.Declare map: docs/proof/blog_evidence_links_v1.md in stablecoin-audit.

Appendix: replica

Map-package CSVs for footprint, switch quantity, and DEX dependency rows might be regenerated from stablecoin-audit:

cargo run – stablecoin-map-package# native solely dependency CSVs, no DefiLlama/Artemis calls:cargo run – stablecoin-map-package – skip-network

This put up was initially printed on my private weblog: https://egpivo.github.io/web3/stablecoins/defi/2026/05/31/stablecoin-map-local-pegs-dollar-rails.html.

The Stablecoin Map: What Crypto’s Money Rails Rely On was initially printed in The Capital on Medium, the place persons are persevering with the dialog by highlighting and responding to this story.

{kind=link}