When RWA buying and selling turns into a clear service, which elements of the trail cease being seen?

The analogy I hold coming again to isn’t that RWA is one other subprime commerce. It’s about abstraction. Earlier than the monetary disaster, many consumers didn’t examine mortgage threat mortgage by mortgage. They skilled it via cleaner wrappers: bonds, scores, tranches, yields. The wrapper made the publicity tradable. It didn’t make the underlying debt simpler to examine.

Tokenized and gasless RWA buying and selling creates a smaller model of that audit drawback. You see a ticker, a quote, a steadiness, perhaps a sponsored transaction with no gasoline to signal. Behind that display the fill might come from a public AMM, an aggregator route, platform matching, market-maker stock, a relayer, or an issuer-gated redemption workflow — and in some circumstances no speedy public on-chain occasion at all.

I’m not arguing that gasless is unhealthy. The query is whether or not hiding gasoline additionally hides the place the commerce cleared — and whether or not that path is verifiable on-chain.

Half I checked out what tokenization makes seen: transfers, holder graphs, mint/burn occasions, permissioning guidelines. The asset itself remains to be elsewhere. This piece asks what turns into laborious to see when the commerce is packaged as a service.

Public RWA dashboards (e.g., rwa.xyz) are helpful for finding the market: issuers, asset courses, holders, switch quantity, APY, and combination worth. I take advantage of them as maps, not because the audit itself. As soon as an asset seems to be lively, the tougher query is which execution floor carried the user-facing motion, and which report proves it.

A helpful RWA evaluation software ought to first draw the trail, not rank the asset. ERC-20 standardizes how a steadiness strikes:`totalSupply`, `balanceOf`, `switch`, `approve`, `allowance`, and `transferFrom`, not what the steadiness legally means or which off-chain report is authoritative.

The newer UX layers make this extra necessary, not much less. ERC-4337-style account abstraction can cut up the consumer motion throughout a consumer operation, bundler, and paymaster. ERC-4626 standardizes `deposit` and `redeem` for DeFi vaults, however an RWA redemption can nonetheless sit behind issuer guidelines, eligibility checks, and off-chain data. Intent-based UX goes additional: the consumer states a aim and one other layer chooses the route.

Earlier than I belief TVL, quantity, quote success, or correlation, I need to know what the metric is connected to: a pool, a quote route, a platform ledger, a mint/burn log, a redemption doc, or nothing public sufficient to confirm. This can be a flow-path audit, not a reentrancy audit.

The circumstances under will not be one market. They sit in several RWA buildings and depart proof somewhere else:

PAXG: tokenized gold; every token maps to vaulted bodily gold. On this panel, public AMM swimming pools are the principle on-chain learn.USDY: tokenized yield be aware backed primarily by short-term Treasuries and cash-like property; broader on-chain entry than the fund merchandise under.BUIDL: BlackRock’s tokenized money-market fund; institutional and permissioned on issuance and switch.OUSG: Ondo’s institutional Treasury product; eligibility-gated subscribe and redeem, with permissioned on-chain flows.AAPLx / xStocks: tokenized fairness publicity via a platform interface; platform matching and token-level swimming pools don’t essentially present the identical exercise.

They will all look tradable from the display. I’m not evaluating which is bigger. I’m evaluating the place a commerce or exit leaves one thing inspectable.

The illustration can dwell on-chain. Liquidity formation doesn’t must. I began with public swimming pools: a 90-day panel, cross-product comparability, and that was nonetheless too clear.

The panel window is 2026–03–10 to 2026–06–08 on Ethereum mainnet public swimming pools except acknowledged in any other case. ETH gasoline and BTC absolute returns weren’t meaningfully related to PAXG or USDY pool-volume relationships on this panel. USDC every day switch counts couldn’t be collected reliably, Alchemy `eth_getLogs` responses exceeded dimension limits on each day tried, so funding-rail diagnostics had been left clean slightly than inferred. These null outcomes matter; they don’t seem to be hidden.

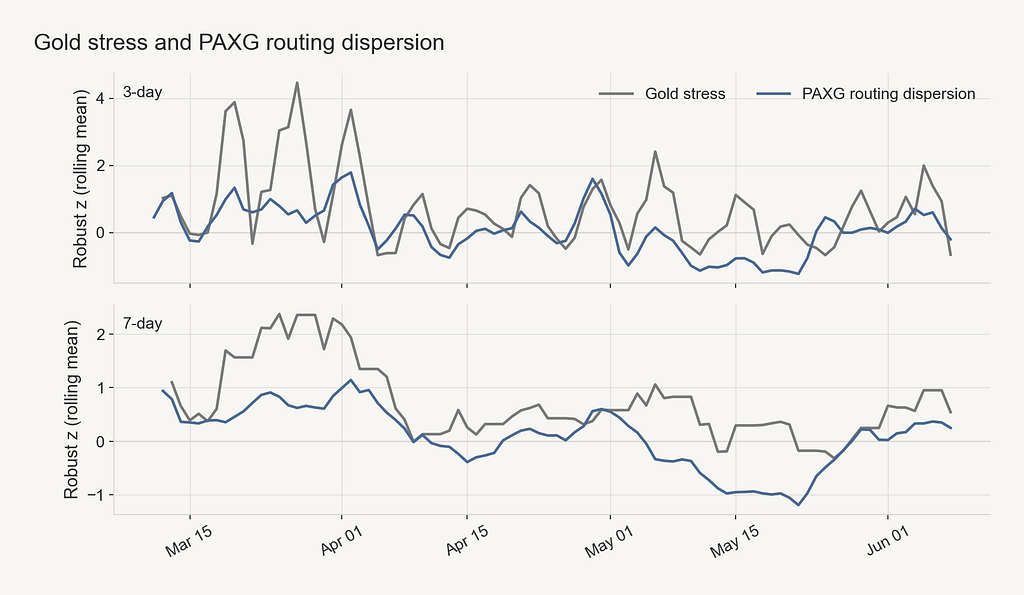

PAXG was the place the reference market really helped

COMEX gold futures and a pool-routing learn can sit on the identical calendar within the 90-day panel.

The core sign is reference stress displaying up in how quantity routed, not in a single headline quantity. Larger gold-reference stress coincided with quantity unfold throughout extra swimming pools in time (gold abs-return z vs dispersion z: r about +0.51, n = 90). When stress rose in late March 2026, public routing seemed much less dominated by the highest pool. That doesn’t show causality; it’s in keeping with broader venue use slightly than flight to at least one pool.

Beneath that sample, the general public floor was lively however fragmented: PAXG confirmed quantity on 91/91 days and about $4.8M median every day quantity, but median top-pool quantity share was nonetheless about 84%. A June 9 cross-section confirmed why reserve TVL alone is deceptive: the highest pool held solely about 27.9% of noticed reserves, far under its quantity share.

Transaction `0xf627…` exhibits the log-level ground: PAXG `Switch`, USDC `Switch`, and a Uniswap V3 `Swap` in a single hash. Weekly ParaSwap route checks returned paths via $100k in any respect 13 checkpoints — aggregator API checks, not accomplished trades.

USDY seemed lively till I requested for dimension

USDY doesn’t present a clear reference-linked response; as a substitute, bursts in public-pool exercise coincide with focus and a quote boundary that didn’t transfer at bigger examined sizes.

USDY pool-volume bursts had been related to greater top-pool focus (quantity strong z vs share strong z: r about +0.49, n = 91). Uncooked top-pool share sat at or close to 1.0 on about 66% of days — a ceiling that makes focus the readable response metric slightly than a unified dispersion scale borrowed from PAXG. Gold, BTC, and ETH gasoline didn’t present significant alignment with USDY pool quantity on this panel. Fragility proxies: quantity CV 1.72 vs PAXG 0.66; spike ratio about 33× vs 5×; median every day quantity close to $1.5k on 89/91 lively days with median lively pool TVL close to $40k.

A public pool can present exercise with out increasing what a holder might really exit at dimension.

The examined route stopped between $10k and $100k: smaller quotes succeeded at each weekly checkpoint; bigger ones didn’t return at any. A failed route response is an API-level boundary on this check setup — not a declare that no off-chain or permissioned exit exists. Ondo major subscribe and redeem workflows are compliance-gated and principally off the general public AMM floor reviewed right here. The cut up nonetheless issues: a swap quote, a pool print, and a permissioned burn will not be the identical proof. Transaction `0x8be2f5…` is a burn occasion — about 49,990 USDY burned, about 56,768 USDC via intermediate contracts — not a Uniswap swap. The Could 22 pool spike is a fragility probe solely, not a sourced demand occasion.

BUIDL and OUSG weren’t pool issues

For BUIDL and OUSG, I didn’t get a helpful pool quote. The learn sat in permissioned mint, switch, and burn logs.

Transaction `0x4aea…` on BUIDL produced 64 logs in a single hash: 32 zero-address mint `Switch` occasions to 32 distinct recipients, 32 non-Switch occasions in the identical transaction, and about 46,016.43 BUIDL minted in complete. BUIDL had successfully no noticed public DEX pool depth at evaluation: settlement seen right here, public swap floor absent. What the logs assist is batch issuance to 32 recipients in a single hash. What they depart open: whether or not every mint displays new subscription money, reallocation, bridge processing, or administrative batching; who funded what; investor identification. No subscription money leg seems within the token occasion log reviewed right here.

Transaction `0x762bcc…` is the distinction in the identical token: a single 980.25 BUIDL `Switch` between allowlisted addresses: motion, not mint workflow. Not each dense BUIDL row is identical enterprise occasion.

On the exit facet, transaction `0x56634c…` on OUSG exhibits about 18,533.97 OUSG burned with about 2.14M USDC transferring via named middleman contracts and returning to the redemption contract inside the similar hash. Burn and stablecoin actions are correlated in a single transaction. Switch logs present USDC biking via intermediaries again to the contract, not a confirmed credit score to the initiating holder’s pockets. OUSG redemption is eligibility-gated per Ondo product documentation. Secondary-holder entitlement, closing payout rail, and authorized impact stay open.

A control-plane learn primarily based on `proprietor()` alone was rejected in evaluation: proxy, admin, and transfer-agent roles want a fuller position map than a single Ownable slot. Chain proof ends the place paperwork and position maps start.

The dashboard row I eliminated

A DeFiLlama BUIDL row of roughly $829M initially seemed like lending liquidity beside empty public swimming pools. Evaluate confirmed it didn’t map to a selected lending market, provided collateral, borrowable liquidity, or a redeemable exit. It was asset/protocol TVL-style knowledge, not a mapped exit. We eliminated it.

A dashboard row can look related whereas describing the improper layer.

AAPLx is the place the interface drawback comes again

Dash sources cited about $1.07B 30-day xStocks platform quantity (platform-wide; per-token cut up not verified). A 2026–06–09 GeckoTerminal examine discovered Solana AAPLx pool TVL close to $215.75k and 24h quantity close to $100.06k.

A consumer can expertise that as one AAPLx market. I couldn’t join a platform commerce to a pool print or a pockets credit score. Commerce-to-chain correlation was not verified right here. When funding or exit strain exhibits up, that is the hole I’d need to hint first: who offers liquidity, and which report proves the fill?

Closing

I don’t belief a single liquidity quantity from this panel. The audit worth isn’t “token on-chain, due to this fact clear.” It’s whether or not the circulate path — exit, stock, sponsor, platform ledger — leaves proof you possibly can examine. The rejected BUIDL row was the warning: a dashboard quantity can look helpful and nonetheless describe the improper layer.

For simplicity, I used linear correlation as a display, not as a conclusion. The 90-day panel can not establish causality. It solely helped me see which surfaces moved collectively, which of them stayed silent, and the place I ought to return to the precise path: quotes, swimming pools, transfers, mint/burn logs, and platform data.

Appendix: replica

Repo: github.com/egpivo/rwa-auditPanel: 2026–03–10 → 2026–06–08; Ethereum public-pool knowledge, COMEX gold reference, ParaSwap quote checks, chosen transaction-log reconstructionsArtifacts: `knowledge/circulate/`; determine scripts in `scripts/plot/`Transaction replay: `cargo run — bin rwa-flow-tx — 0x<tx_hash>Correlations: computed from the saved 90-day panel recordsdata; dwell API re-runs might differ barely.

This publish was initially revealed on my private weblog: https://egpivo.github.io/2026/06/14/where-rwa-trades-and-exits-actually-clear.html

The place RWA Move Leaves Traces was initially revealed in The Capital on Medium, the place persons are persevering with the dialog by highlighting and responding to this story.

{kind=link}