The Each day Breakdown dives into ServiceNow, which regardless of beating on earnings, tumbled after its report and weighed on software program shares.

Concerned about extra Deep Dive content material? Take a look at our newest analysis.

Deep Dive

Simply when it regarded just like the worst could also be behind it, shares of ServiceNow tumbled 17.6% on Thursday. Regardless of beating earnings and income estimates and elevating full-year steerage, buyers punished the inventory amid ongoing issues that its moat might be eroded by AI. That concern isn’t distinctive to ServiceNow — the broader software program area pulled again on Thursday, with many names nonetheless nicely under their 52-week highs even because the Nasdaq 100 has returned to file highs. So what’s the deal?

ServiceNow sells cloud software program that helps enterprises digitize and automate workflows throughout IT, customer support, HR, safety, and different back-office features by means of its Now Platform. It’s more and more embedding AI into that platform by means of Now Help and newer AI brokers, which may energy search, summaries, suggestions, conversational assist, and extra autonomous activity execution inside current workflows.

Regardless of the noise, ServiceNow continues to ship strong development, with income, working earnings, free money movement, and margins all shifting in the appropriate course.

Future Development Projections

Even with the corporate’s robust monitor file and spectacular development expectations over the following a number of years, buyers stay uneasy in regards to the potential disruption from AI. It creates a traditional Wall Avenue conundrum: Is that this merely an overreaction to an unfounded concern, or are sellers accurately getting forward of a long-term downside?

Based on Bloomberg, analysts undertaking the next:

Earnings Development: 19.3% in 2026, 20.1% in 2027, and 18.7% in 2028

Income Development: 20.9% in 2026, 21.6% in 2027, and 18.3% in 2028

Analysts presently have a consensus worth goal of ~$149 on NOW inventory, implying about 74% upside to at this time’s inventory worth.

Wish to obtain these insights straight to your inbox?

Enroll right here

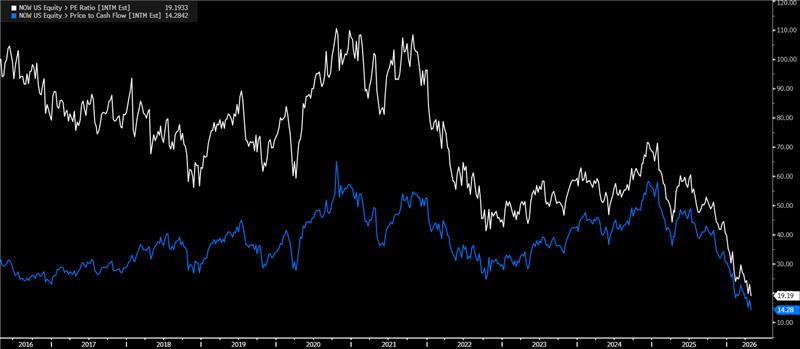

Diving Deeper — Valuation

As a result of ServiceNow’s enterprise continues to develop whereas the inventory continues to fall, the valuation has turn out to be much more approachable. The truth is, on each a price-to-earnings and price-to-free-cash-flow foundation, it has by no means been decrease:

Dangers

In Q1, we took a Deep Dive into software program shares and mentioned the influence AI is having on the group. Whereas many of those corporations could have defensible moats — and whereas many could in the end profit from AI — one of many largest dangers is valuation compression. Put one other manner, a significant re-rating throughout the trade can weigh on inventory costs even when the underlying companies are nonetheless performing fairly nicely.

ServiceNow can also be not insulated from broader financial or macro-related pressures. Working example: the corporate stated geopolitical turmoil within the Center East delayed a number of massive on-premise offers in Q1. Whereas a few of these offers have since closed within the first few weeks of Q2, the disruption delayed roughly $200 million in income final quarter.

The Backside Line

ServiceNow’s underlying enterprise continues to indicate strong development, and the inventory’s valuation has turn out to be notably extra cheap after a steep decline of roughly 50% over the previous yr. On the identical time, bettering valuation and powerful fundamentals alone don’t assure the inventory has bottomed, notably as buyers proceed to weigh AI-related disruption danger, broader software program re-rating pressures, and macro uncertainty.

Disclaimer:

Please word that as a consequence of market volatility, a few of the costs could have already been reached and situations performed out.

Value Prediction 2026, 2027-2030")

Worth Prediction 2026 2027 2028")

? A Newbie’s Information to the Main Privateness Coin")

eyes 0 amid constructive derivatives information")

{kind=link}