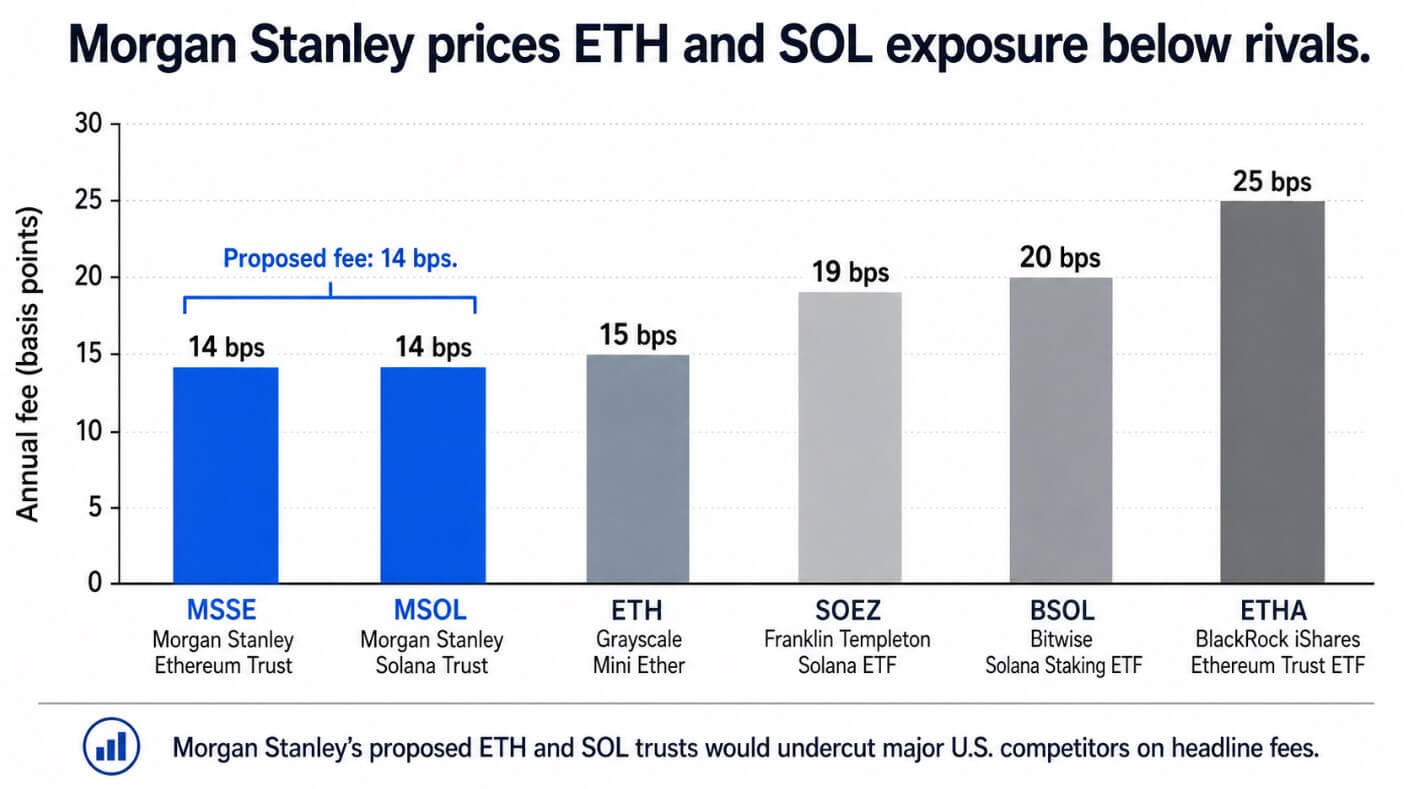

Morgan Stanley filed amended registration statements for proposed Ethereum and Solana ETF trusts on June 18, setting a 0.14% annual delegated sponsor payment on each merchandise.

Bloomberg senior ETF analyst Eric Balchunas described the proposed payment because the lowest amongst ETH and SOL merchandise worldwide.

The ETH belief, anticipated to commerce on NYSE Arca beneath the ticker MSSE, intends to trace ether and staking rewards from a portion of its holdings. The SOL belief (MSOL) intends to stake as much as 100% of its Solana.

BlackRock’s iShares Ethereum Belief ETF (ETHA) carries a 0.25% sponsor payment, Grayscale’s mini Ether (ETH) product sits at 0.15%, Bitwise’s Solana staking ETF (BSOL) launched at 0.20%, and Franklin Templeton’s Solana ETF (SOEZ) lists a 0.19% web expense ratio.

The filings are preliminary, and the SEC should declare each registration statements efficient earlier than shares commerce; neither submitting has reached that threshold.

The payment as a place

Morgan Stanley’s 14 foundation factors on a crypto ETF is a press release about the place the agency expects the institutional allocation dialog to go.

Bitcoin ETFs resolved the entry drawback for establishments, with BlackRock’s IBIT crossing $70 billion in belongings beneath administration inside 18 months of launch.

The following query for wealth managers and advisors is whether or not ETH and SOL, packaged cheaply and reliably sufficient, can occupy a second line in a digital asset sleeve alongside Bitcoin.

Morgan Stanley’s 0.14% payment positions these merchandise as portfolio-building blocks earlier than the allocation query has a broadly accepted reply.

The ETH belief intends to stake 50% to 80% of its holdings beneath regular market circumstances, with staking service suppliers and custodians receiving an anticipated combination 5% of rewards and the belief retaining the rest.

The SOL belief extends that mannequin additional, permitting as much as 100% of holdings to be staked beneath the identical 95% trust-retention construction, with the delegated sponsor explicitly receiving no portion of staking rewards.

Utilizing Bitwise’s disclosed contemporaneous gross staking reward fee of 6.28% as a market benchmark, a completely staked SOL product that retains 95% of rewards would generate roughly 5.97% earlier than the 14 bps payment.

For ETH, at a hypothetical 3% gross staking yield with 50% to 80% staked, the retained staking contribution lands between roughly 1.29% and a couple of.14% after charges.

Advisors evaluating these merchandise are evaluating fee-minus-staking economics, such because the gross yield, the staked share, and the belief’s 95% retention fee, which collectively decide the efficient value of publicity.

ProductHeadline feeStaking shareTrust reward retentionIllustrative retained yield earlier than feeIllustrative web after feeMorgan Stanley ETH Trust0.14percent50%–80% of ETH95percent1.43%–2.28percent1.29%–2.14percentMorgan Stanley SOL Trust0.14percentAs much as 100% of SOL95percent5.97percent5.83%

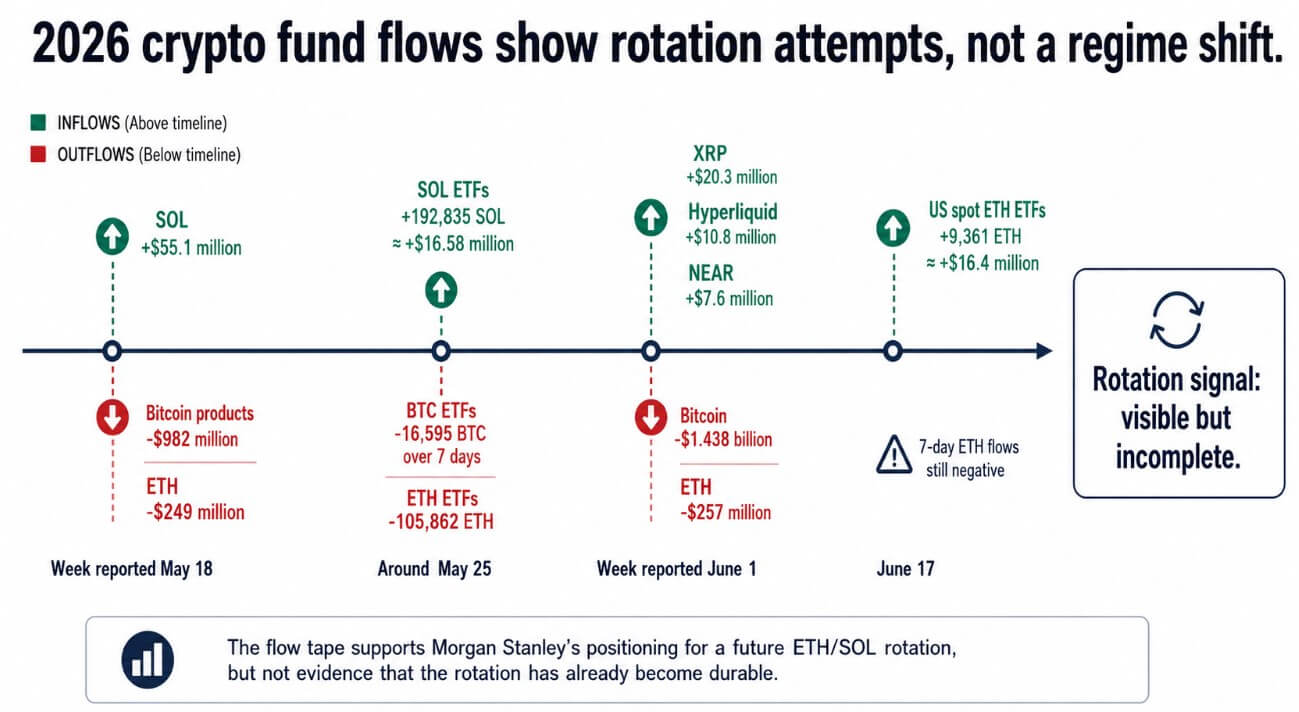

What the circulate information helps

Institutional rotation into ETH and SOL has occurred in matches and begins all through 2026, with episodic demand and no sturdy regime in place.

CoinShares’ week reported Might 18 confirmed Bitcoin merchandise absorbing $982 million in outflows, whereas SOL drew $55.1 million in inflows and ETH noticed $249 million go away.

Round Might 25, US spot ETF information confirmed BTC ETFs dropping roughly 16,595 BTC over seven days whereas SOL ETFs added 192,835 SOL, roughly $16.58 million, as ETH ETFs shed 105,862 ETH.

By the week reported June 1, BTC noticed $1.44 billion in outflows and ETH $257 million, whereas the constructive pockets have been XRP at $20.3 million, Hyperliquid at $10.8 million, and NEAR at $7.6 million.

On June 17, US spot ETH ETFs posted a single-day influx of 9,361 ETH, roughly $16.4 million, with seven-day ETH flows nonetheless unfavourable at week’s finish.

The sample throughout these weeks is SOL selecting up episodic demand whereas ETH lags behind Bitcoin’s personal outflow tempo, with alt-specific bids touchdown on XRP and Hyperliquid, and the ETH/SOL pair failing to draw a sustained bid as a unit.

Morgan Stanley is positioning for a rotation that the information present as episodic and incomplete. The financial institution operates throughout 42 nations, and Morgan Stanley Funding Administration reported roughly $1.8 trillion in belongings beneath administration or supervision as of Sept. 30, 2025.

That distribution attain means a 14 bps payment can be a bid for advisor shelf area. When a wealth supervisor at a Morgan Stanley department decides so as to add non-Bitcoin crypto publicity, MSSE and MSOL are already priced to win the comparability.

Two timelines for a similar wager

The bull case requires 4 or extra weeks of mixed ETH and SOL inflows alongside Bitcoin flows turning flat, with SOL weekly inflows shifting from tens of hundreds of thousands towards a whole lot of hundreds of thousands.

If that rotation arrives, 14 bps turns into a structural weapon: rivals working at 0.19% to 0.25% face the selection of chopping charges or ceding market share to a model with Morgan Stanley’s distribution attain.

A completely staked SOL product retaining 95% of rewards at 14 bps makes the economics in opposition to a 20 bps unstaked competitor troublesome to justify on the numbers alone.

The bear case is that the macro backdrop retains establishments in Bitcoin-only or cash-equivalent exposures longer than the product submitting timeline anticipates.

The Fed held the coverage fee at 3.50% to three.75% by means of mid-2026, with almost half of policymakers projecting a potential fee hike for the 12 months, and inflation forecasts revised larger.

In that surroundings, the allocation case for ETH and SOL as portfolio parts faces a tighter cost-of-capital argument than it did in 2024.

Low charges and staking yields require an allocation case that advisors can justify to the consumer earlier than inflows materialize.

The SEC’s effectiveness timeline provides a separate procedural layer of uncertainty: staking therapy, custody preparations, and tax dealing with may all require additional amendments earlier than both product trades.

The prize Morgan Stanley is competing for is advisor shelf area within the allocation cycle that follows Bitcoin normalization.

By the point establishments broadly settle for ETH and SOL as portfolio-eligible, Morgan Stanley crypto ETFs with low charges and staking pass-through may have a structural first-mover benefit.

![From T+1 to T+0: What Occurs When Put up-Commerce Goes On-Chain [Stable Summit New York Fireside Recap]](https://entethalliance.org/wp-content/uploads/2026/06/Gemini_Generated_Image_lhquhblhquhblhqu.png "From T+1 to T+0: What Occurs When Put up-Commerce Goes On-Chain [Stable Summit New York Fireside Recap]")

{kind=link}