Have you learnt how a lot time you spent watching TV this previous week? I’ll let you know exactly. You spent two hours a day simply on Netflix, and doubtless some extra on YouTube too. Most firms can do considered one of two issues nicely. They will develop quick, or they’ll make some huge cash. Doing each, yr after yr, is uncommon. The best way Netflix manages the battle in your consideration is the rationale I’m not only a long-time subscriber, however a long-time shareholder too.

How does Netflix do it? It has one of many deepest buyer lock-in results on the earth. Netflix raises its costs. Subscribers grumble, a number of cancel, after which virtually all of them keep, as a result of for the cash there may be nothing else prefer it.

The corporate takes that cash and reinvests it into making the platform extra priceless with extra content material, and that permits it to lift costs once more in a virtuous cycle. Then it does it once more the following yr.

This interprets superbly to working metrics. Working margin has gone from 27% to just about 30% to a guided 31.5%, roughly two factors a yr, three years operating. That’s pricing energy and working self-discipline working collectively, and it’s the coronary heart of why I believe Netflix is a top quality enterprise. However there’s a key query that’s scaring buyers away. Netflix guided for decrease income development this yr than the yr earlier than.

If development is slowing from its golden period, does the inventory value replicate a future that’s now not actual?

After Netflix’s current fall, I consider it does. But it surely’s not that easy.

Should you discover this sort of evaluation helpful, think about subscribing. I publish new posts each week.

What Netflix Really Does

Netflix sells leisure. To be exact, it sells streaming leisure to greater than 325 million paying households, reaching an viewers approaching a billion individuals. You pay a month-to-month payment, you get an enormous library of movies and sequence in dozens of languages, and more and more you’ll be able to pay much less if you happen to settle for some advertisements.

The cash is available in 3 ways.

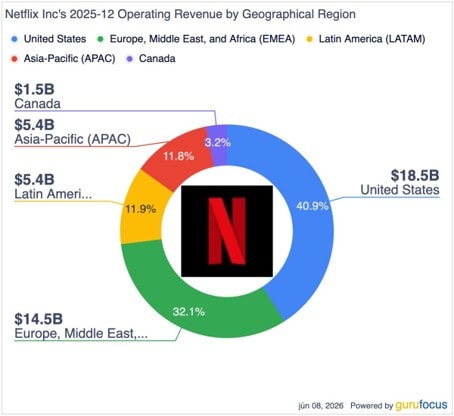

Most of it’s subscriptions, cut up throughout 4 areas: the US and Canada (the largest by income), Europe (the largest by members), and the faster-growing Latin America and Asia-Pacific.

The second stream, nonetheless small however rising quick, is promoting on the cheaper ad-supported plan. The third, newer nonetheless, is dwell occasions: NFL video games, massive boxing matches, the World Baseball Basic, weekly WWE.

Did the quantity originally shock you? It’s true. The typical member watches about two hours a day, and in late 2025 Netflix reached its highest-ever share of TV time within the US, at 8.6%. This reveals how fierce the competitors in your consideration is, and it additionally reveals how a lot runway Netflix has forward of it.

Why I’m Writing About Netflix Now

Netflix was having fun with a large bull run, however that every one modified with a shocking administration resolution. The normally prudent, underpromising and overdelivering administration tried to amass WBD, a legacy film studio with huge real-world belongings. Precisely the sort of agency Netflix has been placing out of enterprise.

Traders punished the corporate instantly. The inventory fell from $130 to $75. The bull thesis seemed damaged. Till one thing sudden occurred. Paramount joined the struggle, and ultimately received the bidding warfare and bought WBD.

The outcome? Not solely did Netflix stroll away from an unpopular acquisition, nevertheless it additionally acquired a $2.8 billion break-up payment. The query is, now that the elephant within the room has been addressed, what continues to be protecting the inventory value depressed?

Netflix is quietly shifting its narrative. It was a subscriber-growth story. In 2025, Netflix stopped reporting that quantity solely. It was clear Netflix wished to redefine itself, and for buyers to have a look at income, revenue, and engagement because the platform matured and needed to pivot to pricing and supplementary enterprise strains to drive outcomes, not simply subscriber development. Which means development now comes as a lot from elevating costs and scaling advertisements as from including members. The advert enterprise doubled in 2024, grew about two and a half occasions in 2025, and is focused to roughly double once more to round $3 billion in 2026.

The Numbers That Matter

Income grew about 16% in 2025 to $45 billion, and is guided to roughly $51 billion in 2026. That’s slower than Netflix’s hypergrowth previous, however it’s on a a lot greater base. What issues is that Netflix has been constantly increasing its margins.

Netflix can also be good at producing money. Free money movement went from about $6.9 billion in 2024 to about $9.5 billion in 2025, up 37%. Virtually all of that money goes towards shopping for again inventory.

The Moat

Netflix’s aggressive benefit comes from its sheer scale of content material. Pricing energy is the proof. Netflix can increase costs even in a weaker shopper setting as a result of, for the cash, it delivers probably the most leisure per hour. That hole between worth and value is the moat.

The opposite moat mechanism is scale. Netflix spreads a content material finances of roughly $16 billion throughout 325 million households. That lets it each outspend opponents on hits and nonetheless broaden its margin. Higher economics carry higher content material, which drives engagement, which funds extra content material.

Is the moat sturdy? I believe Netflix can widen its content material moat, however it’s contested on whole consideration share, the place it competes not solely with YouTube but additionally with different platforms like Disney+ and Prime Video.

The Aggressive Panorama

The streaming trade, with Disney, Amazon, Apple, and the newly merging legacy gamers, poses an actual menace. However due to a years-long first-mover benefit, Netflix has entrenched itself throughout the vast majority of the addressable market.

Netflix has to win on content material breadth, as a result of its opponents have inherent benefits on high quality, comparable to Disney motion pictures and HBO reveals. However to this point, the corporate has managed this nicely.

Dividends & Buybacks

Netflix doesn’t pay a dividend, by selection, and has been clear it has no plans to begin. As a substitute it returns basically all of its free money movement by means of share repurchases: about $6.3 billion in 2024 and $9.1 billion in 2025, steadily shrinking the share rely. With free money movement rising and a $2.8 billion one-time payment within the financial institution, I count on the buyback to proceed.

Bull Case / Bear Case

The Bull Case

The bull case assumes Netflix would compound on each axis directly. It might develop income within the mid-teens, proceed elevating costs whereas protecting retention regular, scale the high-margin advert enterprise, and broaden working margin additional on higher value economics. The bull’s trustworthy danger is value: the standard is well-known.

The Bear Case

The bear case rests on development expectations. Netflix’s valuation rests on the belief that it will likely be capable of develop and broaden margins. There’s already a slowdown in income development, and since Netflix stopped reporting subscriber numbers, we are able to deduce that subscriber development might be slowing too. Nonetheless, at this value, Netflix is priced for low single-digit development, one thing I think about unlikely.

If you realize somebody who’d discover this convenient, sharing goes a good distance.

Valuation & What the Road Thinks

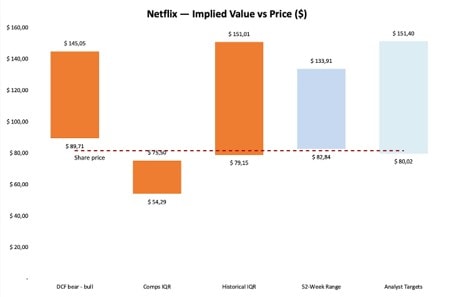

Netflix has traditionally traded at a premium valuation, which is why wanting purely at historic valuation might be deceptive.

I worth portfolio firms based mostly on three lenses. The historic valuation, if one have been to count on the agency to revert to its long-term median. The peer valuation, taking a look at how the market values related firms, adjusted to replicate the interquartile vary to strip away extremes. And a customized DCF mannequin, the place I mannequin the financials towards my expectations of future efficiency.

I take advantage of Wall Road analyst targets and the 52-week buying and selling vary as a sanity test.

As you’ll be able to see, Netflix is now buying and selling on the low finish of its historic valuations, analyst estimates, and its buying and selling vary.

Its friends commerce cheaper, however the reason being that Netflix lacks actual pure-play streaming friends to match towards. My DCF valuation suggests a ground of $90 if the enterprise continues to carry out according to expectations.

In investing, it is very important use a margin of security, and for a higher-risk title like Netflix, I like that margin to be 20% beneath truthful worth. That brings us to a good worth estimate of $101, representing a 24% upside from the present value.

The draw back I’d think about an actual danger is a reversal to the $75 assist, the place I’d revisit the thesis.

From a fast technical perspective, Netflix is presently sitting at an necessary assist degree. If this breaks, we are able to count on one other down leg to $75, at which level, if the thesis and the financial system haven’t shifted dramatically, I’d think about including considerably.

Netflix has already proven it has the momentum to recuperate towards a extra affordable value, however that fizzled out after the newest earnings report.

My Take

I lately purchased extra Netflix inventory. It presently makes up round 7% of my portfolio. Netflix has what I search for: a powerful enterprise, pricing energy, and a administration workforce that likes to underpromise and overdeliver.

On the draw back, I’d reassess my thesis if margin enlargement stalls or a value improve lastly drives subscribers away.

Backside Line

Netflix grows within the mid-teens, raises costs with out dropping prospects, expands its margins yearly, and generates near $10 billion in money it fingers again to shareholders. The enterprise is firing on each cylinder. The one actual debate is what it’s value. Whether or not it belongs in your portfolio depends upon the value you pay and your time horizon, however I believe the machine itself is value maintaining a tally of.

I share all my strikes in actual time on eToro, the place over 1 500 buyers comply with my portfolio. Should you’re curious how this matches into the larger image, come discover me there: https://www.etoro.com/individuals/thedividendfund

Thanks for studying R² Funding Membership! Subscribe totally free to obtain new posts and assist my work.

This communication is for info and training functions solely and shouldn’t be taken as funding recommendation, a private suggestion, or a proposal of, or solicitation to purchase or promote, any monetary devices. This materials has been ready with out bearing in mind any specific recipient’s funding goals or monetary state of affairs and has not been ready in accordance with the authorized and regulatory necessities to advertise unbiased analysis. Any references to previous or future efficiency of a monetary instrument, index or a packaged funding product are usually not, and shouldn’t be taken as, a dependable indicator of future outcomes. eToro makes no illustration and assumes no legal responsibility as to the accuracy or completeness of the content material of this publication.

The submit The Missed Tech Big You Shouldn’t Ignore appeared first on eToro.

{kind=link}