Vitalik Buterin is difficult considered one of DeFi’s most acquainted security mechanisms: the automated liquidation that closes a debt-backed place when collateral falls under the required backing for the mortgage.

In a June 1 Ethereum Analysis put up, Buterin proposed constructing artificial, index-tracking property on prime of choices, with collateralized debt faraway from the bottom design.

The concept would take away the laborious liquidation set off from the bottom design and substitute it with a slower type of threat: the person’s publicity drifts away from the goal until the place is rebalanced.

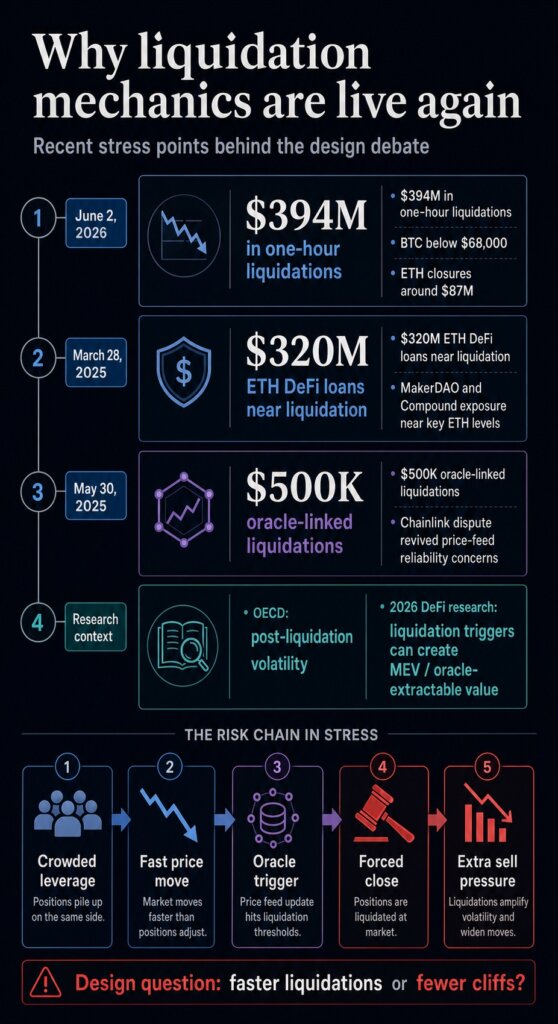

That distinction is essential as a result of the outdated mechanism continues to be displaying up in market stress. Bitcoin‘s fall under $68,000 triggered about $394 million in one-hour liquidations on June 2, together with roughly $87 million in ETH positions, as leveraged bets had been force-closed throughout the market.

The flash crash got here someday after Buterin’s put up and serves as a market reminder: when value strikes hit crowded leverage, computerized closures can flip a drop right into a wider market occasion.

The proposal is research-stage structure: a design argument separate from any protocol launch, Ethereum roadmap dedication, or direct alternative for Aave, Maker, or present stablecoins. It shifts the main focus from collateral buffers and sooner value feeds to a extra basic design alternative: whether or not instantaneous liquidation ought to stay DeFi’s central technique of surviving a crash.

Why the protection swap can amplify stress

Most DeFi lending programs are constructed across the identical fundamental drawback. A person locks in collateral, borrows towards it, and should hold the place above a required security degree.

In Aave’s borrowing documentation, that degree is expressed by a well being issue. When it falls under 1, the place could be liquidated: a liquidator repays debt on the borrower’s behalf and receives collateral plus a bonus.

That construction protects the protocol’s solvency, but it surely additionally concentrates motion on the worst potential second. If ETH or one other collateral asset falls quick sufficient, customers don’t select when to promote. The system chooses for them.

Liquidators compete to shut eligible positions, and the collateral could be pushed into markets already quick on liquidity.

The report helps that concern. An OECD working paper on DeFi liquidations discovered a optimistic relationship between liquidation exercise and post-liquidation value volatility throughout main decentralized trade swimming pools.

The paper additionally emphasised that liquidators depend on obtainable liquidity throughout stress, which suggests the mechanism designed to revive stability can run into the identical liquidity scarcity as everybody else.

CryptoSlate has beforehand coated the operational model of that threat. A 2025 Chainlink-related oracle dispute led to greater than $500,000 in liquidations on Euler Finance and revived questions on how protocols ought to interpret pricing knowledge in illiquid markets.

Individually, a 2025 ETH decline put almost $320 million in Ethereum-based DeFi loans inside 20% of liquidation, with MakerDAO and Compound publicity concentrated close to key value ranges.

The widespread thread is the cliff. DeFi wants a technique to deal with undercollateralized positions, however the present methodology typically waits till a quantity is breached after which requires instant motion.

That creates a crowded second for debtors, liquidators, oracle feeds, and liquidity suppliers concurrently. It additionally provides subtle actors a transparent set off to observe, as a result of the protocol rule declares when a place turns into worthwhile to shut.

For customers, the sensible consequence is easy. A liquidation system can defend a lending pool whereas nonetheless giving the person borrower the worst potential execution window.

The person could have meant to maintain long-term ETH publicity, hedge a money want, or wait out a pointy wick. As soon as the brink is crossed, the system’s precedence turns into solvency, and the person’s timing choice disappears.

How choices flip a cliff into drift

Buterin’s different begins by altering the primitive. A place that may change into undercollateralized provides technique to a cut up ETH declare: the proposal divides 1 ETH into two option-like property, known as P and N, tied to a value index, strike value, and maturity date.

At maturity, an oracle resolves the index worth and determines how a lot of the ETH declare both sides receives.

The important thing property is easy: P and N all the time add again as much as 1 ETH. As a result of the system is dividing a set ETH declare between two sides, it might keep away from seizing collateral from a borrower to shut a deficit.

In Buterin’s framing, the design removes the liquidation occasion by development.

For a person making an attempt to carry artificial greenback publicity, the sensible expertise differs from a debt-backed stablecoin. Within the debt mannequin, a person can seem totally hedged till the collateral threshold is breached, at which level the place is force-closed.

Within the choices mannequin, the holder avoids the sudden shut, however the place can steadily cease behaving because the person meant.

Buterin’s instance makes use of a person who desires some degree of greenback publicity whereas ETH is buying and selling round $2,500. The person may purchase a deep choice tied to a decrease strike, similar to $1,500, and rotate into lower-strike choices if ETH falls towards the unique strike.

If the person doesn’t rebalance, the publicity drifts. The person retains a declare, however the hedge turns into much less precise.

That’s the central tradeoff. The design retains threat within the system, and modifications who controls the timing and what type the harm takes.

Liquidation-based programs outsource the choice to a protocol rule and liquidator bots. The choices-based design pushes extra of that call towards customers, wrappers, market makers, or automated rebalancing programs.

Buterin additionally acknowledged a restrict for stablecoin use. A medium quantity of annualized drift could also be acceptable for somebody looking for value stability relative to future bills.

It’s a lot much less helpful for an accounting stablecoin, the place customers need to deal with the token as a greenback for funds, bookkeeping, or tax reporting.

The oracle tradeoff

The oracle argument often is the proposal’s most essential protocol-design declare.

Debt-backed liquidations rely upon real-time value feeds. A protocol wants a binding value shortly sufficient to find out when a place is unsafe and to permit liquidators to behave.

Buterin argues that this constraint makes real-time oracles laborious to safe as a result of they depend on automated actors watching dwell alerts and go away little room for slower dispute decision.

Choices transfer the essential oracle name to maturity. Oracle threat stays, however the time stress modifications.

If a system can wait to resolve a contract, it might use slower, extra contestable mechanisms, together with prediction-market-style approaches or costly fallback oracles that may be impractical for fast liquidation.

That’s the reason the proposal is greater than a stablecoin tweak. It shifts DeFi’s threat structure away from a single dwell value that may set off irreversible motion.

Current analysis on liquidation dynamics in DeFi exhibits why that floor is central: liquidation mechanics can create incentives round value manipulation, MEV, and oracle-extractable worth when a worthwhile closure will depend on a market value crossing a set off.

The profit nonetheless will depend on implementation. A wrapper that mechanically rebalances for customers may make the product simpler to carry, but it surely may additionally recreate seen timing guidelines that subtle merchants can anticipate.

A purely native person agent may cover some timing selections, however would increase its personal usability and execution questions. An onchain DAO wrapper would want deterministic guidelines and deep markets to keep away from turning into one other predictable goal.

Gradual oracles assist provided that the remainder of the design avoids forcing the identical drawback elsewhere. That’s the stress Buterin’s put up leaves for builders.

A slower oracle can provide a system extra time to settle disputed info, however customers nonetheless want markets deep sufficient to rotate publicity and guidelines sturdy sufficient to keep away from turning each rebalance into an exploitable sign.

The comparability with prior oracle disputes is helpful right here as a result of the danger arises when dangerous knowledge meets a rule that should act instantly.

The choices design reduces the necessity for that instantaneous choice, whereas builders nonetheless should determine who watches the index, who gives liquidity, and who absorbs losses when the market strikes sooner than the hedge.

What builders nonetheless should show

The subsequent take a look at is whether or not the market construction round Buterin’s concept could be aggressive with the debt programs it will problem.

The proposal itself flags slippage as a serious threat. Rebalancing by strange automated market makers may very well be costly, particularly if customers have to rotate choice publicity repeatedly throughout unstable intervals.

Buterin instructed that rebalancing may want a unique market construction, nearer to affected person one-sided market making than an instantaneous promote.

That requirement is the adoption take a look at. If customers keep away from liquidation however bleed an excessive amount of worth by drift, slippage, or operational complexity, the mannequin turns into elegant analysis slightly than helpful DeFi infrastructure.

If builders could make rebalancing low-cost and fewer uncovered to assault, the thought may change into a critical different for customers who need value stability with out signing up for a liquidation cliff.

The identical take a look at applies to stablecoin framing. The proposal is most defensible when described as a technique to maintain a stability-oriented publicity or private hedge.

It turns into weaker if marketed as a easy greenback alternative. A token that drifts away from its goal and wishes periodic rotation is a unique person promise from a redeemable greenback, an overcollateralized stablecoin, or a traditional CDP-backed artificial.

For Ethereum, the importance is that considered one of its most influential designers is treating liquidation as an architectural alternative slightly than an unavoidable reality of DeFi.

The subsequent sign is whether or not any protocol crew turns the choices mannequin right into a examined wrapper, simulation, or dwell market with adequate liquidity to reveal the trade-off in follow.

Till then, the proposal is finest learn as a direct problem to DeFi’s crash mechanics: the business can hold making an attempt to make liquidations sooner and higher collateralized, or it might take a look at designs constructed with out sudden pressured gross sales.

{kind=link}