The best way cash strikes by way of the monetary system has modified rather a lot in just some years. Funds are actually quicker, extra versatile, and fewer tied to the sluggish banking programs that used to regulate world finance. Stablecoins deal with billions of {dollars} in transactions daily, blockchain networks can ship worth throughout borders in seconds, and tokenized monetary programs are starting to problem conventional cost strategies. It’s protected to say the world is experiencing a monetary revolution.

Europe is paying nearer consideration as a result of this transformation creates each a chance and a rising strategic concern. Greenback-backed stablecoins like USDT and USDC already dominate massive components of the digital asset financial system, reinforcing the affect of the US greenback in rising monetary infrastructure. Europe faces rising strain to make sure the euro stays related in a world the place worth could ultimately transfer extra by way of tokenized networks than by way of conventional banking programs.

That is the place the Single Euro Funds Space (SEPA) comes into the dialogue. A rising concept is that integrating tokenization into SEPA funds may assist make euro-based digital funds quicker and extra aggressive within the on-chain monetary system. The larger query is whether or not integrating tokenization into Europe’s cost system can strengthen the euro’s world position earlier than digital greenback programs transfer too far forward.

Why SEPA Issues to Europe’s Monetary System

SEPA is one in all Europe’s greatest monetary integration tasks designed to make euro funds throughout taking part nations work as easily as native financial institution transfers. Earlier than SEPA, cross-border funds inside Europe have been usually slower, costlier, and extra difficult as a result of totally different nations used totally different banking programs and requirements.

SEPA solved this by making a unified framework for euro funds. Companies and shoppers may ship cash throughout borders utilizing the identical standardized guidelines and processes, making transfers quicker, cheaper, and simpler to handle. This additionally helped strengthen commerce and monetary integration throughout Europe.

For the European Central Financial institution (ECB), SEPA is not only a cost software. Additionally it is a method for Europe to keep up financial sovereignty, which means it retains better management over its personal monetary infrastructure moderately than relying closely on overseas programs.

Because of this tokenization is changing into strategically necessary to Europe. Integrating tokenized funds into SEPA may assist modernize Europe’s cost rails whereas making certain the euro stays related within the world monetary system.

Why the ECB Is Pushing Onerous for Tokenized Funds

So what’s the ECB’s stance on SEPA funds?

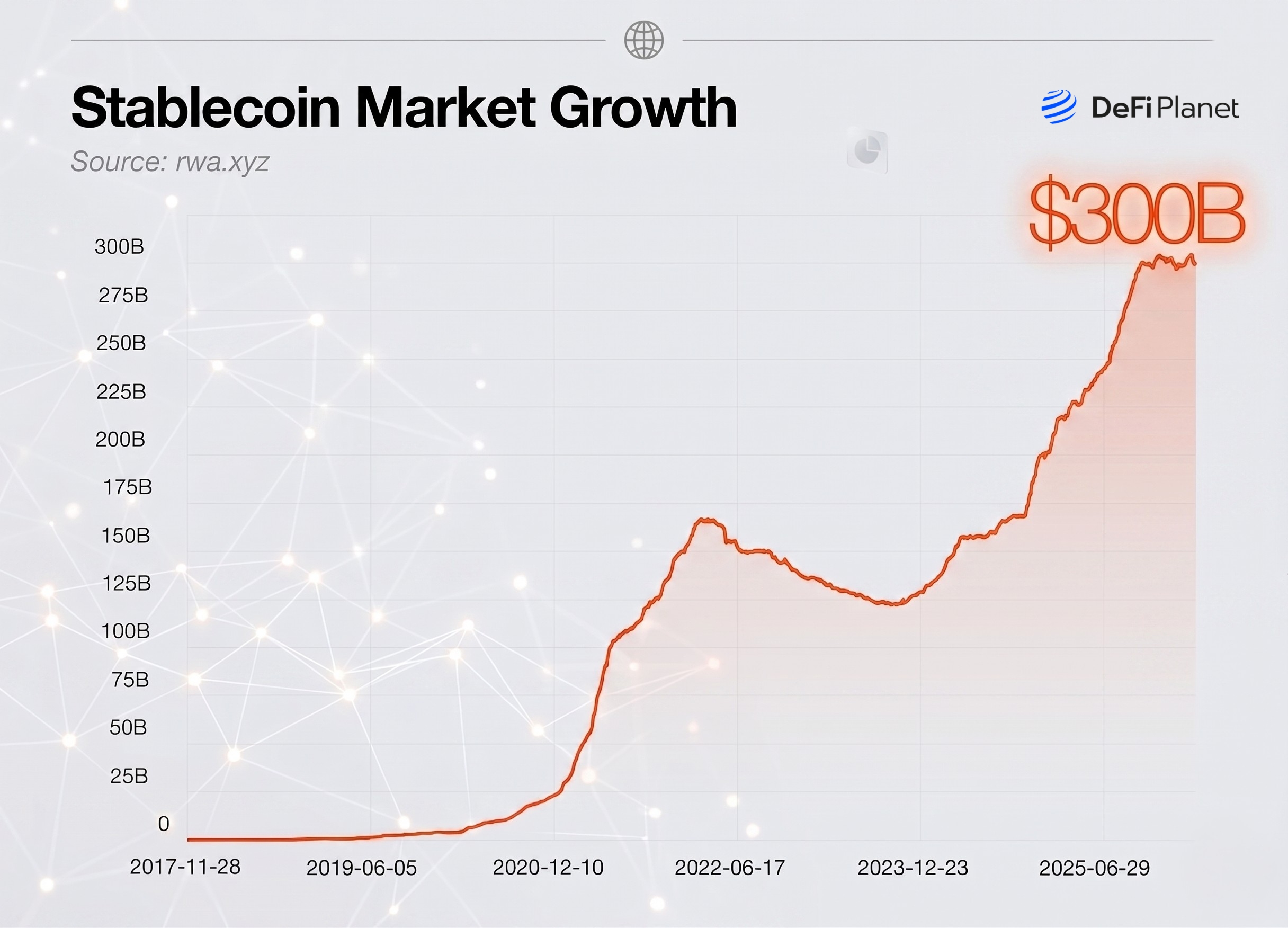

The ECB is paying shut consideration to how briskly digital cash programs are evolving. One key concern is the fast rise of stablecoins, particularly US dollar-backed ones like USDT and USDC, which collectively management over 85% of the stablecoin market.

The overall stablecoin market is now price round $300 billion, making it a significant a part of world crypto liquidity.

Whereas these property usually are not official central financial institution cash, they’re more and more used for cross-border transfers and crypto buying and selling, successfully appearing as a “bridge forex” in world funds. This raises considerations that settlement exercise may steadily shift away from conventional euro-based programs.

The ECB’s fear is not only about competitors, however management. If extra world funds settle in personal stablecoins as an alternative of euros, it may steadily cut back the euro’s position in worldwide finance. In different phrases, even when folks nonetheless use euros in Europe, world digital flows may begin to run on dollar-linked programs as an alternative.

Tokenized funds are seen as a method to answer this transformation. By representing cash and deposits on blockchain-based programs inside regulated European infrastructure, settlement can stay inside supervised monetary rails moderately than shifting to personal, offshore networks. This retains extra cost exercise inside the European system, whilst expertise modifications.

Past technique, tokenization additionally solves sensible issues. It may pace up funds, cut back delays in cross-border transfers, and allow transactions to run 24/7 moderately than solely throughout banking hours. It additionally makes funds programmable, which means cash can transfer routinely when circumstances are met, and it improves interoperability between banks and monetary establishments that at the moment use totally different programs.

Chiara Scotti’s Argument for Tokenized SEPA Funds

Financial institution of Italy Deputy Governor Chiara Scotti has develop into one of many key voices pushing Europe to take tokenized funds extra significantly. In a current speech at a workshop on ‘Digital Property and Financial Coverage Transmission’ held in Rome, she argued that Europe shouldn’t wait too lengthy earlier than modernizing cost programs like SEPA for the tokenized financial system.

Scotti believes Europe ought to actively discover tokenized SEPA funds as a technique to modernize monetary infrastructure whereas nonetheless conserving the euro on the middle of European funds. As a substitute of permitting personal stablecoins to develop into the default digital cash layer, Europe may create tokenized cost rails linked to regulated banks and central financial institution settlement programs.

One among Scotti’s greatest considerations is preserving the euro’s competitiveness in a world the place digital funds have gotten extra world and blockchain-based. If companies and customers more and more settle transactions in dollar-backed stablecoins moderately than euro-based programs, the euro may slowly lose affect in digital commerce and worldwide finance.

The deputy governor additionally warned about fragmentation. Proper now, many tokenized cost programs are growing individually throughout banks, stablecoin issuers, and blockchain networks. With out coordination, Europe may find yourself with disconnected programs that don’t work easily collectively. Scotti argues that Europe wants interoperable infrastructure so tokenized funds can transfer throughout establishments with out breaking the “singleness” of cash.

One other main level in Scotti’s argument is the significance of conserving central financial institution cash related in tokenized finance, as belief in cash in the end is determined by trusted establishments and settlement programs. If extra monetary exercise strikes onto blockchains, Europe needs that system to stay anchored to regulated banking infrastructure and central financial institution settlement moderately than absolutely shifting towards personal digital currencies.

Appia’s Function in Europe’s Lengthy-Time period Tokenization Technique

The ECB’s Appia undertaking is a part of Europe’s broader plan to organize its monetary system for a tokenized financial system. The undertaking is tied to the ECB’s wider technique of constructing an built-in digital monetary ecosystem by round 2028, the place tokenized property, digital funds, and blockchain-based settlement programs can function inside regulated European infrastructure.

The primary purpose is to create a framework that enables totally different types of digital cash to work collectively safely. This consists of tokenized financial institution deposits, stablecoins, and central financial institution cash current inside the identical monetary surroundings as an alternative of competing in utterly separate programs.

One main focus is interoperability. Europe needs banks, cost suppliers, and monetary platforms to have the ability to trade tokenized property and funds easily throughout networks. And not using a frequent infrastructure, tokenized finance may develop into fragmented, the place every establishment runs remoted programs that can’t simply join with others.

Appia additionally displays Europe’s try to stop personal stablecoins from changing into the dominant settlement layer for digital finance. By creating infrastructure that retains settlement linked to regulated monetary establishments and central financial institution programs, Europe hopes to keep up financial management whereas nonetheless supporting innovation.

The undertaking’s significance spans past simply funds as a result of tokenization may ultimately have an effect on a lot wider components of finance. Tokenized programs could later be used for bonds, securities, commerce finance, collateral administration, and cross-border settlement.

Is Appia Already Fixing the Downside?

Appia straight addresses many considerations raised by Chiara Scotti as a result of its whole purpose is to maintain Europe’s monetary system linked to central financial institution cash whereas getting ready for tokenized finance. The undertaking focuses closely on interoperability, frequent requirements, and decreasing fragmentation between banks, tokenized deposits, and digital settlement programs.

Nonetheless, main gaps nonetheless stay. Appia’s full blueprint will not be anticipated till 2028, whereas personal stablecoin issuers and US-linked digital cost programs are increasing globally a lot quicker. Europe additionally nonetheless faces challenges round interoperability between totally different DLT networks, fragmented authorized frameworks throughout member states, and slower institutional decision-making.

The chance is that by the point Europe absolutely builds its tokenized infrastructure, dollar-backed stablecoins could already be deeply embedded in world digital funds and settlement flows, making it tougher for euro-based programs to catch up.

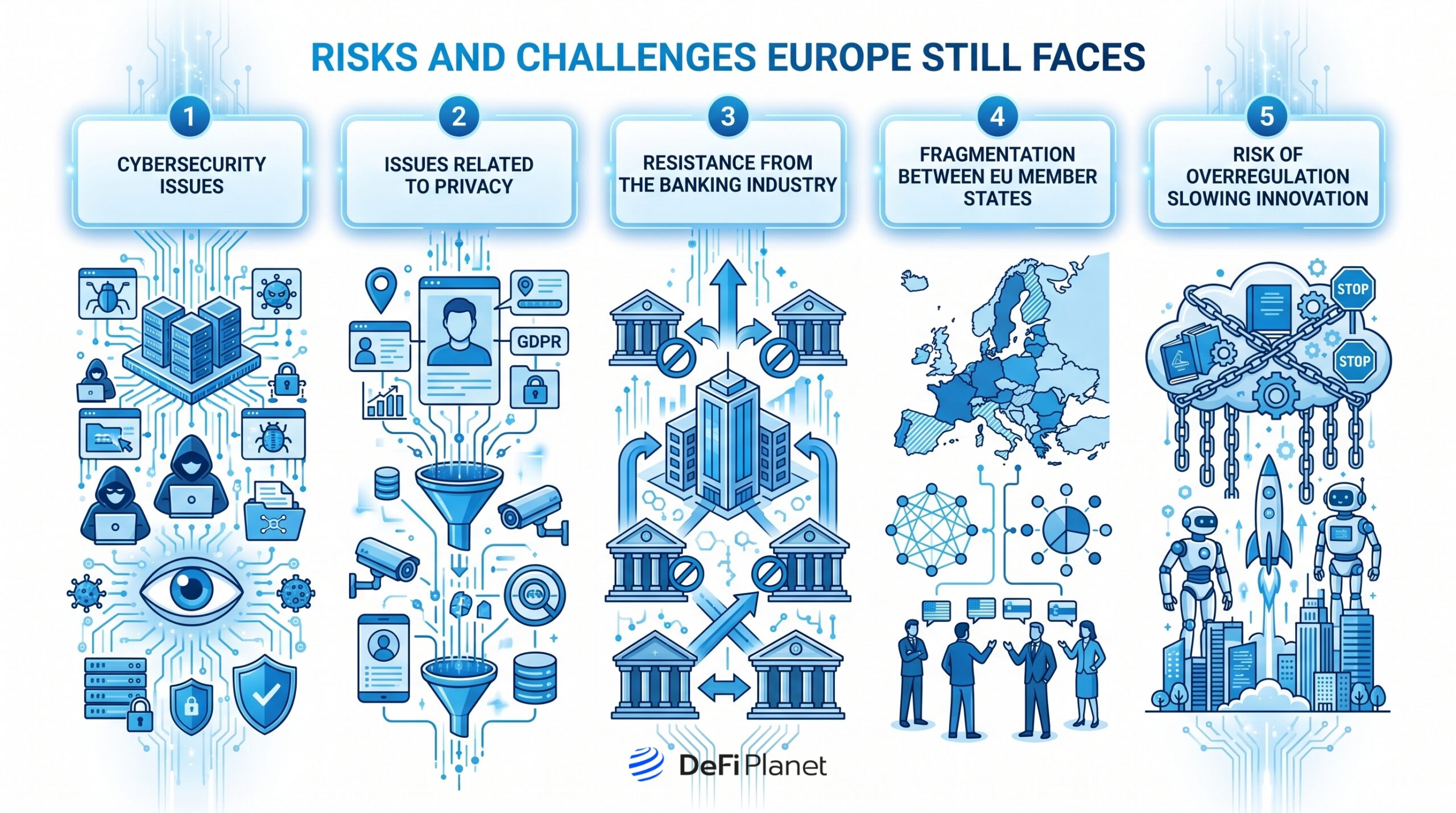

Dangers and Challenges Europe Nonetheless Faces

Though tokenization of SEPA funds can be helpful in enhancing the European monetary sector, the next challenges proceed to hinder this area:

Cybersecurity points

With an rising pattern in direction of digitalizing and utilizing blockchain for funds, there might be elevated publicity to cyber assaults. Such assaults on cost infrastructure, in the event that they happen, can undermine public confidence in Europe’s digital cost undertaking.

Points associated to privateness

With reference to transaction monitoring, tokenization of funds can be an enormous benefit, however on the identical time, it creates privateness points for end-users. Specifically, European regulators are striving to realize a correct stability between monetary monitoring and the safety of private monetary data. Whereas it is very important develop options that shield in opposition to fraud and monetary crimes, customers on the identical time should not really feel as if they’re being monitored on a regular basis.

Resistance from the banking business

Conventional banks would possibly resist utilizing tokenization expertise, even silently, attributable to its potential to undermine their management over funds and their settlement. In circumstances the place prospects have a chance to make transactions quicker than earlier than utilizing tokenization or every other fintech companies, then banks will lose a few of their energy over the cost course of.

Fragmentation between EU member states

Whereas SEPA has managed to standardize euro-based transactions, there’s nonetheless fragmentation with regards to authorized and regulatory variations between totally different nations inside Europe. This might decelerate Europe’s potential to compete with extra centralized programs growing within the US or Asia.

Threat of overregulation slowing innovation

Europe has lengthy been acknowledged as essentially the most tightly regulated continent with regards to monetary transactions, however these days, the specter of overregulation is rising stronger due to the attainable hindrance that it’d deliver to improvements. If the issuance of tokenized monetary merchandise turns into too difficult within the area, it will make logical sense for companies to seek out greener pastures.

Glimpsing Into the Way forward for Digital Finance in Europe

Tokenized SEPA funds is a sound milestone in growing a digital finance system in Europe, which doesn’t routinely suggest abandoning conventional cost programs in favour of innovation.

With correct use of tokenization expertise, Europe would possibly simply be capable to mix each worlds, i.e., develop a extra environment friendly cost community whereas preserving connections to the present system of cash transfers.

The primary drawback lies to find the optimum stability between innovation, supervision, monetary stability, and aggressive place within the worldwide monetary market. Whereas Europe want to encourage innovation in monetary applied sciences, it nonetheless wants to keep up tight regulation and shopper safety.

Too sluggish progress on this case will go away the area open to the dominance of American stablecoin issuers and overseas fintech companies, whereas overly fast developments could entail varied dangers for each banks and monetary markets.

In any case, the results of this delicate stability could have an effect on Europe’s world financial energy sooner or later, significantly contemplating the rising recognition of cross-border funds, tokenization of property, and blockchain settlements the world over.

Disclaimer: This text is meant solely for informational functions and shouldn’t be thought-about buying and selling or funding recommendation. Nothing herein needs to be construed as monetary, authorized, or tax recommendation. Buying and selling or investing in cryptocurrencies carries a substantial threat of economic loss. All the time conduct due diligence.

Loved this? Bookmark DeFi Planet, discover associated matters, and comply with us on Twitter, LinkedIn, Fb, Instagram, Threads, and CoinMarketCap Group for seamless entry to high-quality business insights.

Take management of your crypto portfolio with DEFI PLANET PRO, DeFi Planet’s suite of analytics instruments.”

{kind=link}